In the news. Patrick Conway, the president and CEO of Blue Cross Blue Shield of North Carolina was arrested and faces charges of driving while impaired and reckless driving after an alleged alcohol-related automobile accident in summer, 2019. In additional, because two minor children were in the car with him, he also faces charges of misdemeanor child abuse.

The arresting officer noted bloodshot eyes, odor of alcohol, slurred speech, and unsteadiness. Conway refused a breathalyzer test and his license was suspended for 30 days.

Conway entered a 30-day inpatient rehabilitation program and was back at the helm of Blue Cross Blue Shield of North Carolina for a limited time.

After the news became a tsunami of headaches for Blue Cross, Conway stepped down.

Patrick Conway is also a physician with an excellent pedigree.

Conway completed his pediatrics residency at Harvard Medical School’s Children’s Hospital Boston, graduated with high honors from Baylor College of Medicine [my alma mater], and graduated summa cum laude from Texas A&M University.

Apparently, no one was injured in the fender bender.

My point is not to pile on – but use the example to analyze what happens to the average Joe with a fender bender, a DUI, and an injury. And a giant hospital bill.

Well, it depends.

A DUI is an illegal act. No surprise. Many insurance policies have language that denies coverage for illegal acts.

At least 18 states have laws or regulations relating to illegal act exclusions, according to the National Conference of State Legislatures (NCSL). States allow or prohibit the exclusions in a wide range of insurance policies, including health, life, and long-term care. In addition, the breadth of the exclusion varies significantly among states. For example, California allows a long-term care insurer to deny coverage for “participation in a felony, riot, or insurrection” (Cal. Ins. Code § 10235.8), while Iowa excludes coverage for “any injury incurred during the commission of, or an attempt to commit, a felony or sickness incurred while engaging in an illegal act or occupation or participation in a riot” (Iowa Admin. Code § 191-71.14(8) (38)).

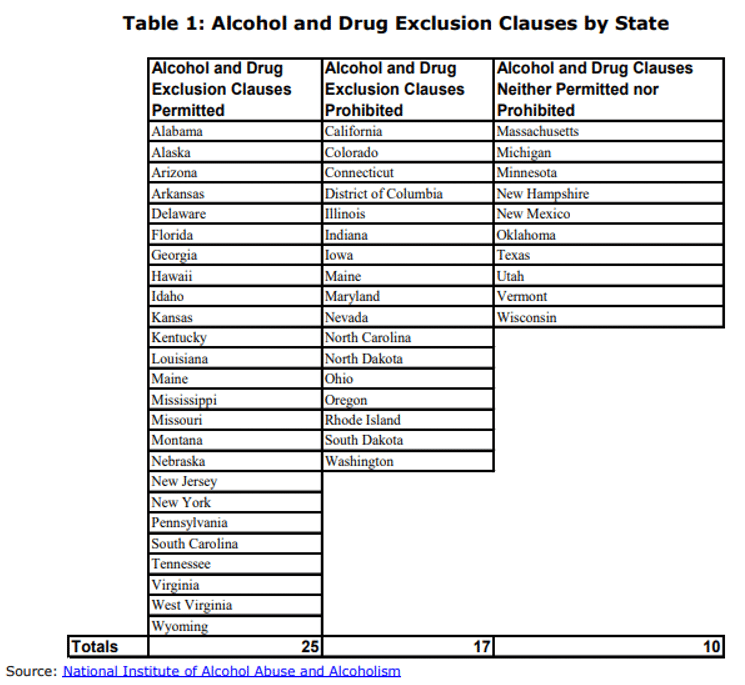

According to the National Institute of Alcohol Abuse and Alcoholism, 25 states explicitly permit drug and alcohol exclusion clauses in health and sickness policies, 16 states and the District of Columbia explicitly prohibit such clauses, and 10 states do not have provisions explicitly allowing or prohibiting the clauses.

In states that allow denial of coverage for alcohol and drug related injuries, carriers are not required to include such exclusions.

North Carolina, where Patrick Conway leads Blue Cross, prohibits alcohol and drug exclusion clauses.

But, not so fast.

Federal law is silent on excluding such clauses. And many insurance policies are not state based. They are company sponsored and beholden to ERISA, a federal law.

ER physicians are savvy to the problem. They often hold off on even drawing blood alcohol and drug levels if the state allows insurance companies to skimp on paying for treatment of injuries from motor vehicle accidents caused by drugs or alcohol.

Blue Cross Blue Shield of North Carolina, as a self-insured company providing benefits for its employees, would likely be able to skimp on payment for such injuries. Does it do so? I have no idea. But, if it does, it may want to rethink that exclusion.

The original exclusion laws were designed to avoid rewarding bad behavior. The world has changed in the decades since. Almost no one thinks about their health insurance coverage before deciding to have drinks and get into their car. So, the only benefit today is to save a carrier some cash and stiff doctors who have to treat due to EMTALA. Laws allowing carriers to exclude coverage for drug and alcohol related injuries have outlived their usefulness and should be tossed in all states and federally.

The medico-legal space is full of antiquated legislation. One example is the National Practitioner Data Bank (NPDB). It supplies hospitals, licensing bodies, and credentialing entities with information related to malpractice payments and other adverse actions. As time has passed, the NPDB has morphed into a weapon plaintiff’s attorneys can point at the throats of capable physicians. Many providers have been tarred without merit.

We’ve perfected strategies doctors can use to settle cases, when appropriate, which can avoid reporting to the NPDB. Become a member of Medical Justice to gain access to these strategies – and many more…

What do you think about the case described in this post?

Jeffrey Segal, MD, JD

Chief Executive Officer and Founder

Dr. Segal was a practicing neurosurgeon for approximately ten years, during which time he also played an active role as a participant on various state-sanctioned medical review panels designed to decrease the incidence of meritless medical malpractice cases.

Dr. Segal holds a M.D. from Baylor College of Medicine, where he also completed a neurosurgical residency. Dr. Segal served as a Spinal Surgery Fellow at The University of South Florida Medical School. He is a member of Phi Beta Kappa as well as the AOA Medical Honor Society. Dr. Segal received his B.A. from the University of Texas and graduated with a J.D. from Concord Law School with highest honors.

In 2000, he co-founded and served as CEO of DarPharma, Inc, a biotechnology company in Chapel Hill, NC, focused on the discovery and development of first-of-class pharmaceuticals for neuropsychiatric disorders.

Dr. Segal is also a partner at Byrd Adatto, a national business and health care law firm. With decades of combined experience in serving doctors, dentists, and other providers, Byrd Adatto has a national pedigree to address most legal issues that arise in the business and practice of medicine.

Why is Maine in both columns for ‘prohibiting’ and ‘permitting?’

Michael Trueworthy wrote: Why is Maine in both columns for ‘prohibiting’ and ‘permitting?’

Evidently the legislature was drunk when it wrote the law.

You are right. This does not seem to make sense. Maine legislature adopted a law which differs slightly from the model law.

The insurer shall not be liable for death, injury incurred, or disease contracted while the insured is intoxicated or under the influence of

narcotics or hallucinogenic drugs unless administered on the advice of a physician.

Research did not reveal any case law where an insurance company sought to deny coverage for treatment of a disease contracted while the insured was under the

influence of drugs or alcohol.

So, an example might be a STD contracted while the patient is drunk. Maybe.

Not sure why the summary data I pulled from suggested Maine allows and prohibits insurance exclusions for drug and alcohol injuries. The statute suggests that Maine allows such insurance exclusions.